1st time homebuyers

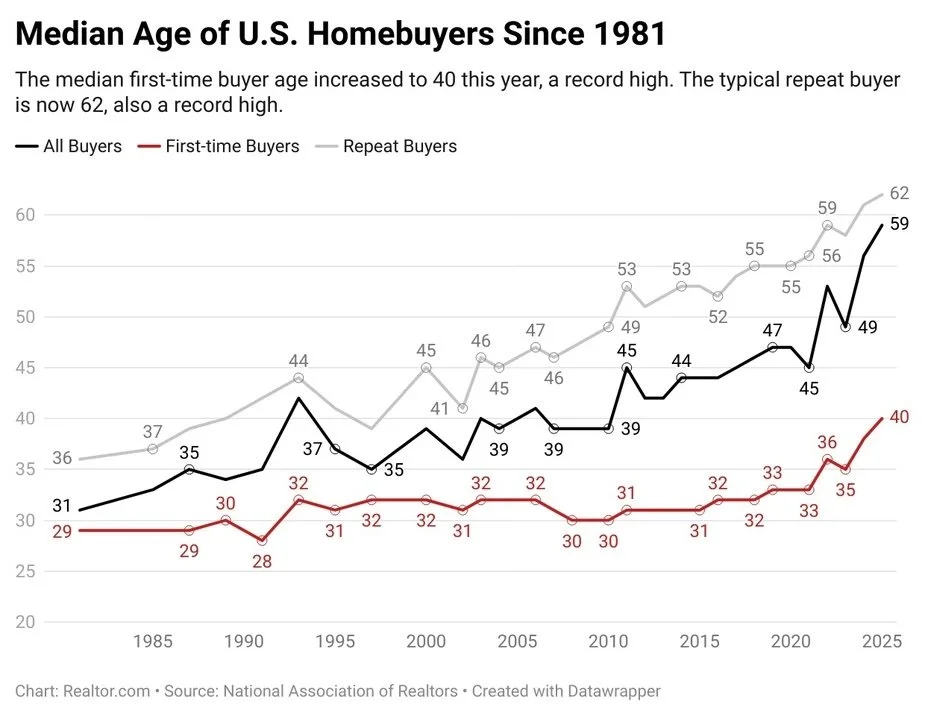

The median age of a first-time buyer in the United States has reached 40, up from 38 a year earlier and a far cry from the early-30s norm of prior decades. For repeat buyers, the median now stands at 62.

The Generational Lockout: Why First-Time Homeownership Now Peaks at Age 40

The National Association of Realtors’ 2025 Profile of Home Buyers and Sellers delivered a milestone few celebrated: the median age of a first-time buyer in the United States has reached 40, up from 38 a year earlier and a far cry from the early-30s norm of prior decades. For repeat buyers, the median now stands at 62. Redfin data show the typical duration of homeownership has fallen to just 11.8 years. These figures underscore a structural shift that has quietly redefined the wealth-building pathway for younger cohorts.

Three interlocking forces explain the delay:

Wage stagnation for the bottom 80 % of earners, largely unchanged in real terms since the 1970s, despite the globalization and offshoring boom that began with NAFTA-era trade agreements.

Unprecedented non-mortgage debt burdens—student loans, auto financing, and childcare—absorbing an ever-larger share of stagnant incomes.

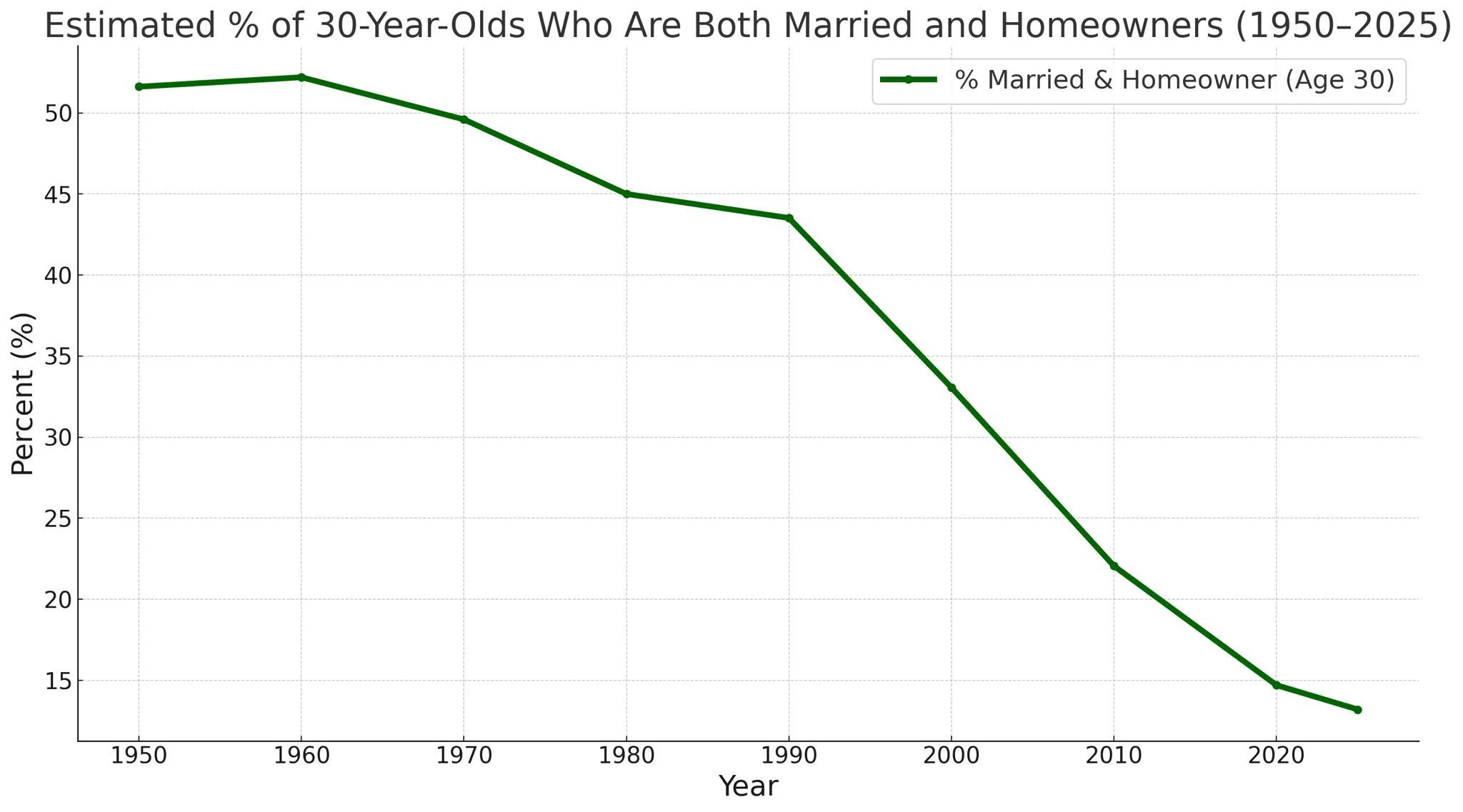

Postponement of traditional milestones: only 12 % of 30-year-olds today are both married and homeowners, compared with more than 50 % in the 1950s.

The consequence is a pronounced rise in intergenerational wealth transfers within the housing market. NAR data indicate that 39 % of all buyers now receive family assistance for down payments; among millennials the figure climbs to 54 %, and among Gen Z it reaches 78 %. Separate research from Northwestern Mutual reveals that more than half of Gen Z and nearly 60 % of millennials now view future inheritances as a core component of retirement security—an implicit admission that organic wealth accumulation through home equity feels out of reach.

“The data point that only 12% of 30-year-olds in the U.S. are both married and own a home originates from analysis by firms like John Burns Research and Consulting and is widely cited by various media and public figures. This statistic is considered credible, reflecting broader data trends from official sources like the U.S. Census Bureau regarding declining marriage and homeownership rates among young adults

• 1950: 50%

• 1960: 52%

• 1970: 48%

• 1980: 45%

• 1990: 43%

• 2000: 35%

• 2010: 25%

• 2025: 12%”

While the 12% figure is likely an estimate based on combining these different data points rather than a single line item in a federal report, it is widely accepted by economists and sociologists as an accurate representation of current trends.

Historical policy choices have compounded the problem. The early-2000s American Dream Downpayment Act and related subprime initiatives contributed to the 2008 crisis and its aftermath of roughly seven million foreclosures. Post-crisis bailouts prioritized financial-institution balance sheets over principal reduction for households. The ultra-low interest rates of the Trump-era pandemic response, in turn, catalyzed the 2020–2022 price surge that has yet to fully unwind.

Enter the latest proposed remedy: the 50-year mortgage. Proponents argue that extending the amortization period reduces monthly payments by roughly 12–14 % compared with a conventional 30-year loan. On a $500,000 loan at prevailing 6.5–7 % rates, the payment drops from approximately $3,160 to $2,632. Lenders, however, are expected to price the longer term with a 42–57 basis point premium (HousingWire/Logan Mohtashami). Over the full term, total interest paid can approach double that of a 30-year note. Given that the median holding period remains under 12 years, the lifetime penalty for most borrowers is mitigated, but the product nonetheless shifts additional interest income to lenders and keeps upward pressure on asset prices.

The broader implication is clear: incremental financial-engineering solutions—whether zero-down programs, extended terms, or shared-equity schemes—have consistently failed to restore broad-based access to homeownership without inflating prices or transferring wealth upward. The most reliable remaining levers for younger households are those under individual control: forming dual-income households, relocating to markets with remaining appreciation potential, and minimizing non-housing debt.

Until supply-side constraints or macroeconomic conditions fundamentally rebalance, the data suggest that age 40 is the new 30 for first-time buyers—and the traditional timeline for building intergenerational wealth through real estate has been indefinitely postponed.